This blog post is sponsored by T. Rowe Price. All thoughts, opinions, and experiences are my own.

My mother was a fierce woman. She left colonial Antigua to pursue midwifery in England back in the 1950s, lived throughout Europe and Canada, and finally settled in New York City in the 1970s with her then-husband to grow a family and live happily ever after.

But when my father abandoned my mother, my brother, and me, to be foot-loose and fancy-free back in Antigua, her world came crashing down and she found herself drowning in depression and disbelief.

When I reflect on my childhood life lessons about money and men, which were rooted in fear, suspicion, and shame, I can’t help but empathize with her pain. But now that I’m a mother to a daughter, I’m committed to making sure Chocolate Drop grows up with something I didn’t have- money confidence.

And so far, we’re off to a great start.

As a five-year-old, she’s learning by example and through direct teaching (y’all know I was a kindergarten teacher, so the explicit instruction is next level… lol.)

Money has many functions, including pleasure and service. Throughout her life, my daughter has had an array of experiences with money. I’ve taken her to the bank to open a savings account for her. I speak to her in age-appropriate ways about the process of depositing and withdrawing money. (She loves doing both).

On top of learning about saving money, Chocolate Drop has had experiences in spending for pleasure: I’ve said yes to many of her requests; I’ve also strategically said no and explained my rationale each time. I consciously expose her to money limits and money abundance, so she knows that both are part of dealing with money.

Plus, she knows that money can be used for international travel, exploring the city, to pay for groceries, to tip, and to pay the meter so we avoid tickets.

Learning about money can be fun. As part of her bedtime routine, I include children’s books that have positive themes and storylines. I look for books that show how families rallied together to save money for a worthy cause, solve a problem, or purchase a special gift for a loved one.

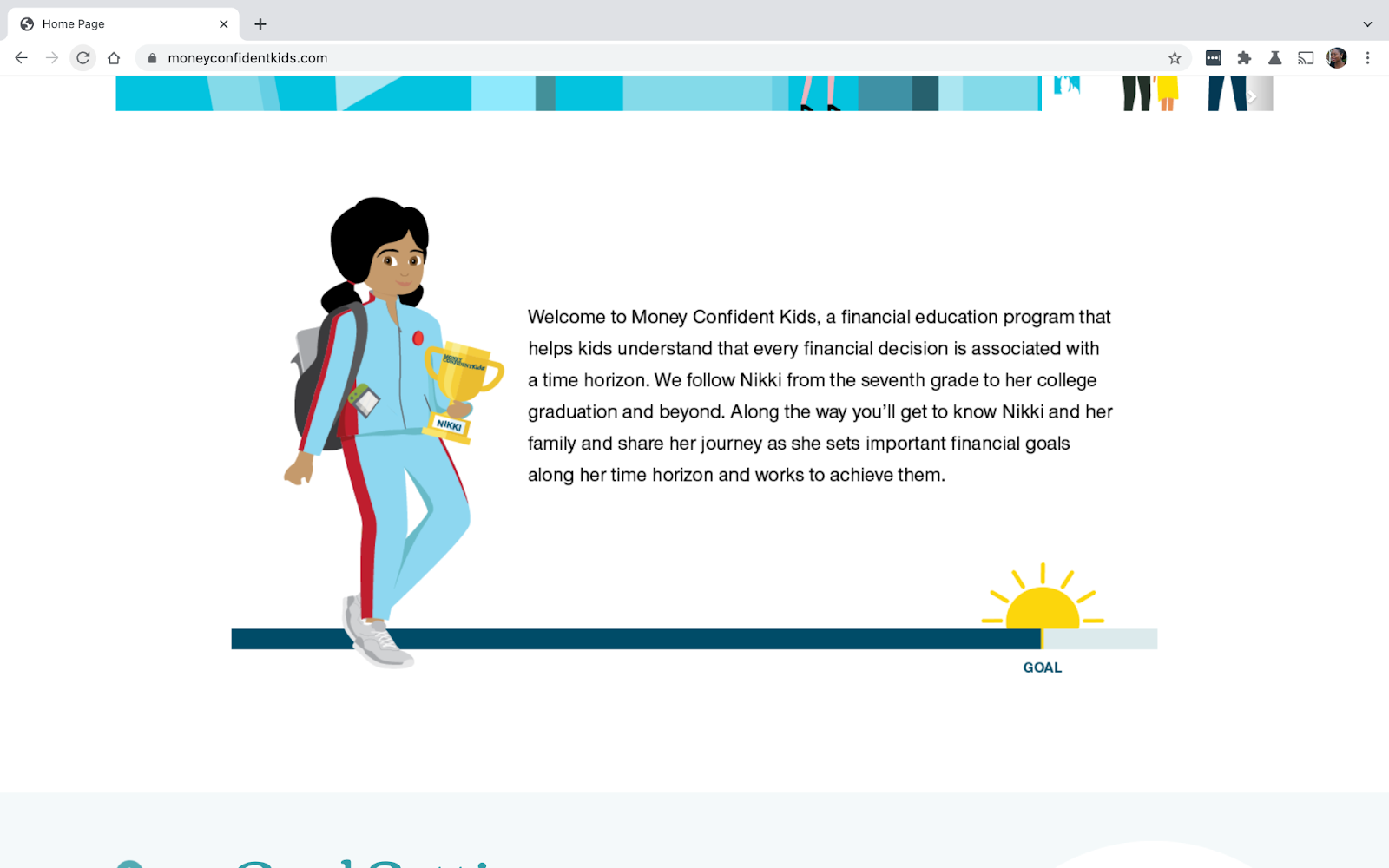

T. Rowe Price’s Money Confident Kids is also an excellent supplement I plan to use to help her learn about the more advanced money topics that usually intimidate adults.

As a personal finance expert and a classroom teacher, Money Confident Kids does an excellent job of explaining topics like value, investing, and risk in kid-friendly language. The lessons on money and inflation, for example, offer thoughtful and easy-to-understand explanations for how inflation affects purchasing power on future purchases. Children will relate to how Nikki, the main character in the curriculum, thinks about saving for expensive purchases in the future like a home, or something fun like a car.

Tough times can create teachable moments. The pandemic rocked our financial worlds. At the onset of COVID-19, I lost income from canceled speaking engagements and brand partnerships. My husband saw a cut in his hours because his company, too, lost clients. Even though she was just a toddler, we explained that some of her favorite places like the daycare and play cafe were closed and may never reopen because the owners didn’t have enough money.

T. Rowe Price’s recent 2021 Parents, Kids & Money Survey found that record numbers of parents across all races have been compelled to hold money conversations as a result of the pandemic. T. Rowe Price recommends that parents discuss money matters with their kids once a week or more. In 2021, a record number of parents followed T. Rowe Price’s recommendation with 47% of parents having money conversations with their kids once a week or more. Since 2017, less than 35% reported following T. Rowe Price’s recommendation each year.

Chocolate Drop is a saver and an investor. Many immigrant cultures drill into their first-generation American children’s heads that saving money is the holy grail and will get you to the land of milk and honey. Conservative money conversations like this also occur in the African American community.

There is some truth to that. Saving money is generally better than spending money. We also want her to learn that saving money alone falls short in helping her grow wealth over time and outpace inflation. In addition to showing her how much money she has in her savings account, I open up her monthly investment statements to show her how her money is growing.

When she’s older, we’ll be able to compare and contrast the growth of both accounts with comparable contributions.

A 529 college fund is bae. Now that she’s in kindergarten, we teach her that college is a “big girl school” and we’re putting money aside every month so she can go without taking on unnecessary debt, learn for learning’s sake, and start her adult life free from the stress of debt. The earlier we start setting money aside, the longer that investment will have to benefit from tax-deferred growth potential. We also automate her savings, so nothing gets in the way of growing her college reserves over the next 13 years.

Our strategy of saving for college now also means that even if we have to borrow for college, we will have to borrow for college less than had we not saved at all. In fact, a T. Rowe Price study showed that borrowing for college instead of saving can potentially more than double total college costs.

Making Money and Happy Memories with My Daughter

I always joke with my friends that if my daughter goes to therapy as an adult, it won’t be because of childhood money issues, lol. I am trying my best to build a kid who is confident about money by equipping her with the experiences, the expertise, and the emotional support to use money as a tool to build the life of her dreams. And for me, it’s worth it!

This blog post is sponsored by T. Rowe Price. All thoughts, opinions, and experiences are my own.